- Browse Category

Subjects

We Begin at the EndLearn More

We Begin at the EndLearn More - Choice Picks

- Top 100 Free Books

- Blog

- Recently Added

- Submit your eBook

- Browse Category

We Begin at the EndLearn More

- Choice Picks

- Top 100 Free Books

- Blog

- Recently Added

- Submit your eBook

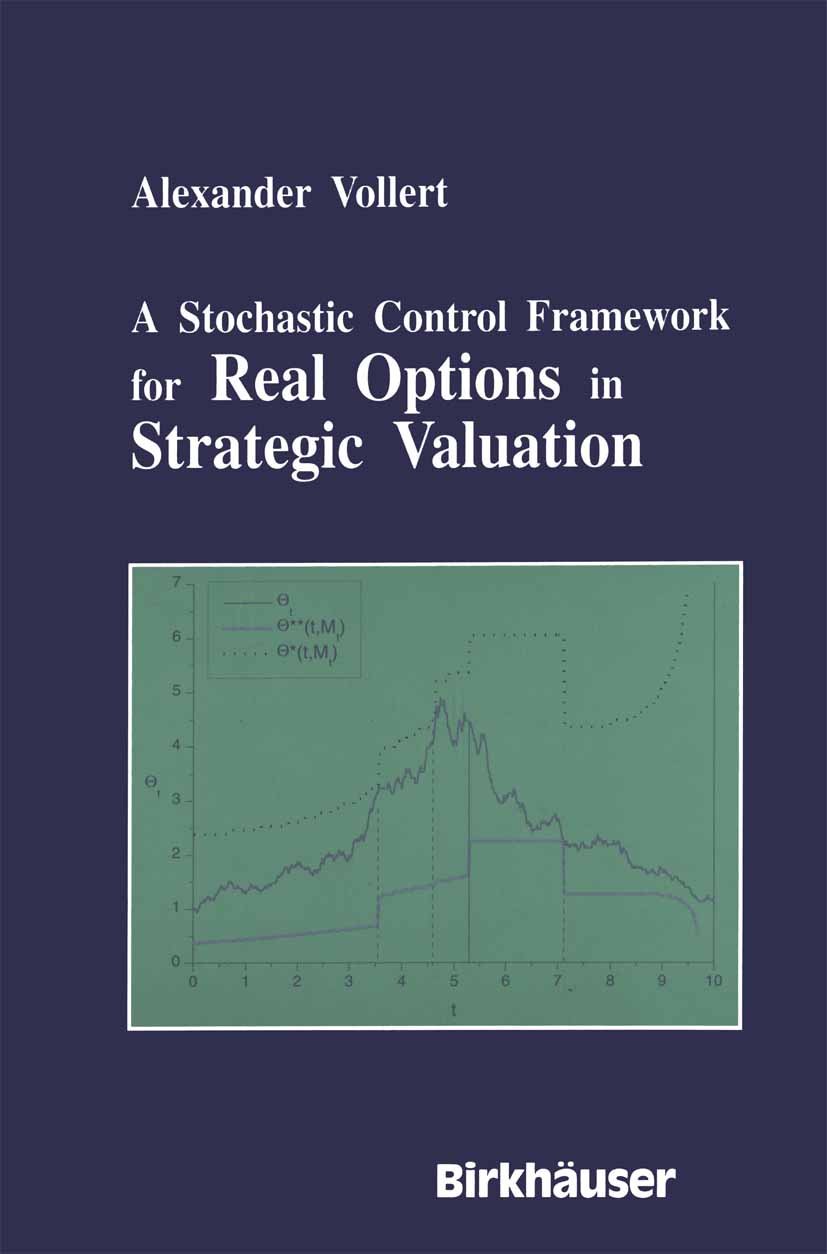

A Stochastic Control Framework for Real Options in Strategic Evaluation

2020-04-19 23:47:12

The theoretical foundations for real options goes back to the mid 1980s and the development of a model that forms the basis for many current applications of real option theory. Over the last decade the theory has rapidly expanded and become enriched ...

Read more

The theoretical foundations for real options goes back to the mid 1980s and the development of a model that forms the basis for many current applications of real option theory. Over the last decade the theory has rapidly expanded and become enriched thanks to increasing research activity. Modern real option theory may be used for the valuation of entire companies as well as for particular investment projects in the presence of uncertainty. As such, the theory of real options can serve as a tool for more practically oriented decision-making providing management with strategies maximizing its capital market value. The book unfolds and examines a new framework for classifying real options from a management as well as a valuation perspective, giving the advantages and disadvantages of the real option approach. Impulse control theory and the theory of optimal stopping combined with methods of mathematical finance are used to construct arbitrarily complex real option models which can be solved numerically and yield optimal capital market strategies and values. Various examples are given demonstrating the potential of the proposed framework.

Less

Compare Prices

| Store | Availability | Book Format | Condition | Price |

|---|---|---|---|---|

| eBooks.com | In Stock | PDF (drm free, digitally watermarked) | PDF (drm free, digitally watermarked) | Buy USD 84.99 |

| Indigo Books & Music | In Stock | Buy CAD 108.67 |

eBooks.comIn Stock

Format

PDF (drm free, digitally watermarked)

Condition

PDF (drm free, digitally watermarked)

Available Discount

No Discount available

Related Books

View All

College Algebra

Solutions Manual to accompany Fundamentals of Matrix Analysis with Applications

Mathematical Modeling and Applied Calculus

Deductive Logic

Introduction to Lie Groups and Lie Algebra, 51

The King of Infinite Space : Euclid and His Elements

Analyzing Longitudinal Clinical Trial Data

Set Theory An Introduction To Independence Proofs

College Placement Math Success in 20 Minutes a Day

The Earliest Arithmetics in English

Intermediate Algebra & Analytic Geometry

Applied Linear Algebra

Topics in Computational Number Theory Inspired by Peter L. Montgomery

How to Think Like a Mathematician

Bayesian Inference for Stochastic Processes

Introduction to Mathematical Philosophy

An Introduction to Generalized Linear Models

Probability

Time Series Analysis with Long Memory in View

A Treatise on Probability

Orthogonal Polynomials and Painlevé Equations

99 Variations on a Proof

Trigonometry Essentials Practice Workbook with Answers

Solving Problems in Geometry

The philosophy of mathematics

Settings

Reflow text when sidebars are open.